Didn't Learn What A Derivative Is In School? Don't Worry-- That Was The Whole Idea

>

This past weekend I went to a symposium set up by the Congressional Progressive Caucus Foundation that featured Barney Frank, chairman of the House Financial Services Committee. Although there were several wonderful Barney moments-- especially the ones where he urged progressives to primary conservative Democrats who vote with the GOP-- he spent most of his time talking about the importance of, and difficulties surrounding, passing strong financial reform regulations. His biggest regret about the bill that passed in the House is that it doesn't tackle derivatives more aggressively, and he said he hopes the Senate-- instead of making the bill weaker, their normal role-- will actually strengthen it. Hard to imagine that happening, particularly with reactionary, corporately owned Wall Street shill Blanche Lincoln in charge of one of the key Senate committees and with the GOP leadership already announcing their intention of obstructing and filibustering the reform efforts.

How can they get away with that, you ask? Well, the stuff is complicated, almost no one understands it, and the GOP message machine will just lie and distort all efforts at reform. Simple. But in case you want to know what it is Blanche Lincoln is doing to water down legislation and what it is Miss McConnell and Jim DeMint are trying to claim is socialistic or fascist or not sufficiently something-or-other, let's turn to our old friend Thom Hartmann and his latest book, Threshold, where he makes derivatives (relatively) simple, through the observations of William Seidman, the chairman of the FDIC appointed in 1989 by George H.W. Bush to run the Resolution Trust Corporation, whose function was to save the nation's savings and loans.

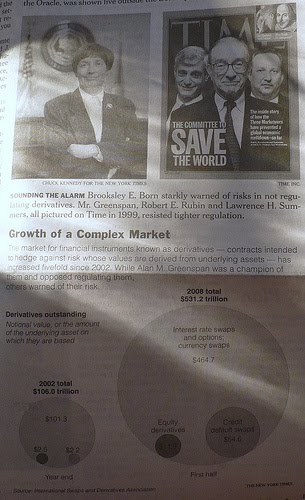

[I]n 2004 the investment banking industry went to the Security and Exchange Commission (SEC), which regulated then, and asked the SEC to abandon their requirement that banks couldn't borrow more than twelve dollars (to buy these tranches-- aggregated subprime loans-- and sell them for a profit) for every dollar they had in capital assets. They argued that the twelve-to-one ratio limit was antiquated, and suggested that they could self-regulate with oversight from the SEC. The SEC, being run by "free market" guys appointed by George W. Bush [corporate shills Harvey Pitt, William Donaldson and Christopher Cox], agreed. As Seidman said, "They [the banks then] went from 12 times leverage to 30 to 35 times leverage." At the same time, the derivative market was developing. A derivative is typically a bet on the future value of a stock or mortgage or some other underlying asset from which its value is "derived." Mortgage insurance-- betting that a mortgage won't fail (a "credit default swap")-- for example, is a form of a derivative.

"The problem was that there was no regulatory agency for these," Seidman said, "and it was proposed that regulation or at least disclosure be required. The industry fought it and the Federal Reserve, under Alan Greenspan, vehemently opposed [transparency or regulation]. I can remember Alan saying, 'Look, these are sophisticated contracts between knowledgeable buyers and knowledgeable sellers, and no regulator can do as well as they'll do, so what do you need a regulator for? The market will regulate these.'

"And he [Greenspan] won the day. Alan was the key person responsible for the fact that we didn't even know how many of those contracts there were, and it was in the trillions."

At the end of his speech, Seidman noted the worldwide crash brought about by the SEC's 2004 deregulation of the banks and the Fed's unwillingness to regulate the derivative market at all, saying that this was "just part of believing that the market will regulate itself if you just let those good people go out there and bargain on their own."

This, of course, is the essence of conservative Law of the Jungle economics. It's nihilistic and revels in creating an unsafe situation for unwary consumers being preyed on by savage and unrestrained predators in fancy suits. Voters may not be completely comfortable with the Wall Street apologists Obama has surrounding him, but they're far from ready to embrace the alternative. McConnell is gambling the farm on being able to trick voters into agreeing to make themselves victims of greedy banksters again and supporting the GOP anti-regulatory positions. This morning, though, Kentucky's populist Attorney General, Jack Conway, who's running for the open Senate seat McConnell pushed Jim Bunning out of, hit back hard against McConnell's pro-Wall Street position:

"As Kentucky small businesses are struggling to get loans and hundreds of thousands of working families are trying to make ends meet all across the Commonwealth, it's outrageous that Senator McConnell is defending Wall Street and threatening to block financial reform regulations,. These tactics are exactly what is wrong with Washington.

"The legislation being considered is an important step toward stopping the excessive greed and risk-taking on Wall Street and Senator McConnell knows it. The American public is angry that it has taken so long for Congress to reign in Wall Street and they won't tolerate any more delays. I support robust financial reform because it will help Kentucky working families by putting consumers first, protecting taxpayers, and preventing financial institutions from ever again becoming 'Too Big To Fail'. If elected to the Senate, I will work to build on this legislation to ensure that Congress is always looking out for Kentucky families before Wall Street and the special interests."

The cookie-cutter Republican shill McConnell is trying to replace Bunning with, Trey Grayson, is being financed by Wall Street and completely supports their assertions that they should be allowed to regulate themselves with no interference from the government. Chris Dodd took to the floor of the Senate to expose McConnell's lies on behalf of the special interests, particularly going after the GOP's Luntz memo. And Bob Reich has a great suggestion for how to deal with shills like McConnell:

Don’t let them get away with it. Smoke the Republicans out. Respond to their criticism that the Dodd bill leaves open the possibility that some future bank will become too big to fail by amending the bill to limit the size of banks to $100 billion of assets-- so no bank can become too big, period. Challenge the Republicans to join you in voting for the amendment. If they decline, force them to explain themselves to their local Tea Partiers.

Labels: Alan Greenspan, derivatives, Jack Conway, predatory capitalism, Thom Hartmann

posted by DownWithTyranny @ 2:00 PM

1 comments

|

Reddit

![]()

![]()

1 Comments:

I blame Adam Davidson at NPR's Planet Money for much of the despairing chorus of "it's all too complicated". THE WHOLE POINT IS TO MAKE YOU THINK THAT ONLY EXPERTS CAN UNDERSTAND IT. If we give up and let these rats regulate themselves, then we're screwed, and we deserve to be.

Post a Comment

<< Home